Ukraine: A difficult situation on the gas front

On 28 March, the state-owned energy company Naftogaz reported a further Russian attack on Ukraine’s gas infrastructure. This was reportedly the eighteenth large-scale strike since the outbreak of the full-scale war and the eighth since the beginning of the year. No specific details of the damage were disclosed, apart from confirmation that the targets were facilities related to gas extraction – most likely, as in previous weeks, compressor and gas treatment stations. The damage was so severe that, in mid-February, Ukraine was forced to increase gas imports nearly tenfold to meet immediate demand.

The situation is further complicated by the fact that current gas reserves in underground storage facilities are at their lowest in at least a decade. This constrains daily extraction capacity and necessitates costly fuel imports. According to the head of OGTSU (the transmission system operator), Ukraine intends to purchase at least 4 billion cubic metres of gas between April and October 2025. A significant portion of this will be American LNG, delivered via EU terminals, including the Świnoujście LNG terminal.

The latest attacks indicate that Moscow is using ceasefire talks with the United States solely as a means to its own ends. It continues to systematically destroy Ukraine’s gas infrastructure, which the Kremlin has exempted from the moratorium on targeting energy facilities (see ‘Negotiations in Riyadh: unclear agreements, slim prospects for implementation’). The principal challenge for Kyiv will be preparing for the forthcoming heating season – most notably, securing sufficient imported gas reserves amid strained public finances.

Commentary

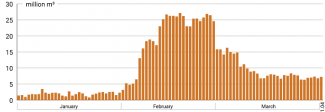

- Over the past few weeks, the nature of Russian attacks on Ukraine’s gas infrastructure has shifted. Rather than targeting storage facilities, strikes have focused on extraction infrastructure – primarily in the Poltava and Kharkiv regions, where the vast majority of gas reserves are located. According to media reports, the attacks in February and March resulted in a 40% reduction in gas output. These losses are indirectly reflected in gas import volumes, which, in the second half of February exceeded 25 million cubic metres per day (see Chart 1) – nearly half of Ukraine’s daily domestic production in 2024. In March, imports were gradually scaled back and stabilised in the second half of the month at approximately 7–8 million cubic metres per day. This suggests that Ukraine has lost approximately 15% of its domestic production capacity for an extended period – although some estimates place the figure higher. In contrast to the electricity infrastructure (see ‘Ukraine: the electricity system is readying itself for Russian attacks’), gas extraction facilities appear to have been left entirely unprotected against drone strikes, or were protected only to a very limited extent. This lack of defence likely accounts for the effectiveness of Russia’s recent operations.

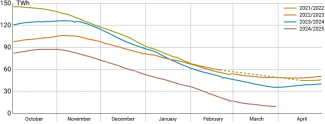

- Gas reserves in Ukraine’s underground storage facilities are at a record low. While Kyiv has not released official data, figures from Gas Infrastructure Europe indicate that, as of 30 March, storage was filled to merely 2.9% of capacity – equivalent to approximately 800 million cubic metres of active gas (9.27 TWh, see Chart 2). Although this amount is sufficient to comfortably close the current heating season – which has already ended in many cities – substantial imports will be required in the coming months. Should Russia persist with effective strikes on extraction infrastructure, the 4 billion cubic metre import target announced by OGTSU may prove inadequate.

- The necessity of significantly increasing gas imports will pose a financial challenge for Naftogaz. While it is difficult to forecast future prices on the European market, based on the past 12 months, the cost could amount to as much as €1–2 billion. Ukraine has already commenced efforts to secure funding, relying on support from international financial institutions and partner states. On 26 March, the European Bank for Reconstruction and Development (EBRD) approved a €270 million loan for gas purchases. On the same day, Norway announced a loan of 1 billion Norwegian kroner (approximately €85 million) for this purpose, along with a €54 million grant.

Chart 1. Daily gas imports since 1 January 2025

Source: OGTSU.

Chart 2. Gas withdrawal from storage, October to April

Source: GIE AGSI+.